NARAYANAN SOMASUNDARAM, Nikkei Asia chief banking and financial correspondent August 23, 2021

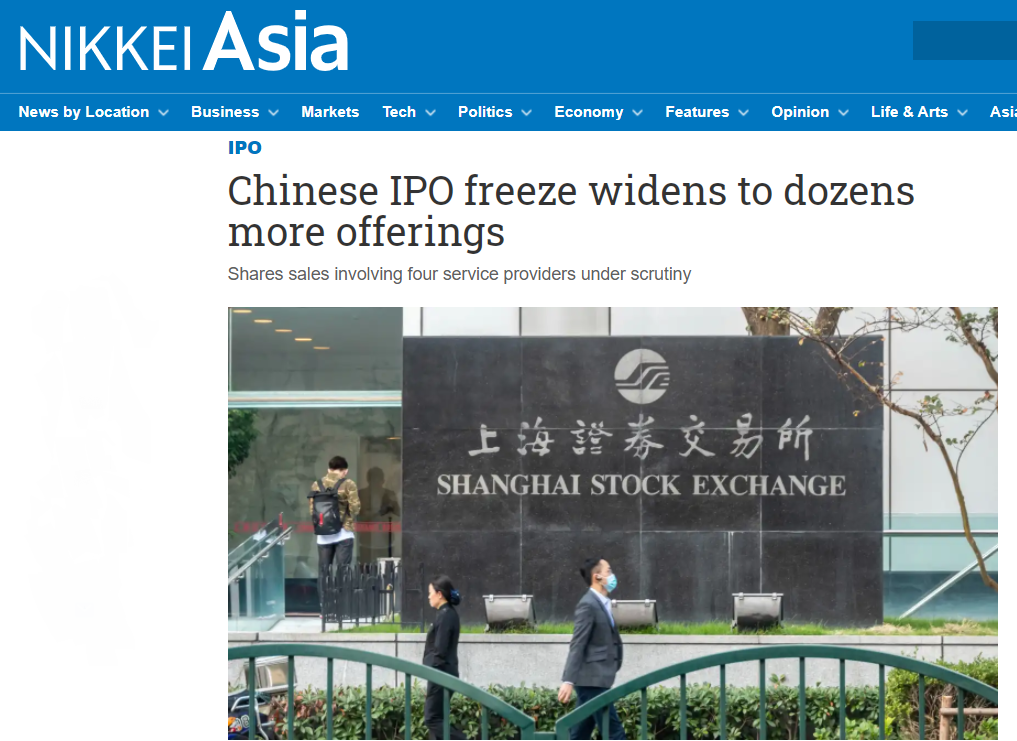

Chinese regulators have frozen more than 40 other IPOs in addition to that of BYD Semiconductor amid a widening investigation into service providers involved with the share sales.

The probe by the China Securities Regulatory Commission focuses on Beijing Tian Yuan Law Firm, broker China Dragon Securities, CAREA Assets Appraisal and Zhongxingcai Guanghua Certified Public Accountants, according to Shanghai Securities News.

The newspaper reported on Monday that 42 initial public offerings on the Shanghai Stock Exchange’s STAR Market or the Shenzhen Stock Exchange’s ChiNext board involving these service companies had been halted, though it did not say what sparked the probe or what investigators are looking into.

In recent weeks, mainland China’s IPO markets have remained active, with China Telecom last Friday raising 54.2 billion yuan ($8.33 billion) as it listed in Shanghai, even as Hong Kong and New York have gone quiet.

The three markets have long been the world’s busiest for IPOs, with Chinese companies driving a major portion of activity in each. However, offshore Chinese IPOs have largely been paused since Beijing rolled out new controls on such share sales in July in the wake of Didi Global’s $4.4 billion New York offering, which some officials had sought to delay.

Some of the new controls relate to data security for technology companies, a sector facing broad scrutiny from Beijing which has wiped out over $1 trillion of market valuation among already-listed companies in recent months.

Some market observers still expect the IPO of the automotive microchip arm of electric carmaker BYD to move ahead later. The company was seeking up to 2.68 billion yuan.

A venture capital fund manager said the offering could be delayed by several months while the company sorts out issues and updates its paperwork, with other halted offerings facing similar delays.

“Probably most or all of the companies will certainly still go public if problems are with service firms, not the companies themselves,” said Peter Fuhrman, chief executive of advisory China First Capital in Shenzhen.

The STAR Market and ChiNext use a “registration” system for IPOs that is intended to be more transparent and quicker than the preapproval system used on the main boards of each exchange.

While the registration system has led to a surge in new listings, the flow has slowed amid tightened controls since the last-minute suspension of Ant Group’s $35 billion IPO, which was shaping up to be the world’s largest, last November.

IPO volumes in the mainland have reached $48 billion so far this year compared with $41.5 billion over the same period last year, according to data compiled by Dealogic. Offerings on the STAR Market have raised $15.3 billion, 36% less than last year, however.

The STAR Market and ChiNext last Friday each issued proposed amendments to their listing rules to enable institutional investors to make higher bids and strengthen supervision of the issuance and underwriting process. Market participants have until Sept. 5 to respond to the proposals.

In a terse statement Thursday, Beijing’s top market regulator, the State Administration for Market Regulation, said it had launched an antitrust investigation into Alibaba. Separately, a joint statement issued by China’s central bank and regulatory agencies overseeing securities, banking and insurance said they would meet with Ant to urge the firm to implement financial regulations and other rules.

Taken together, the actions mark Beijing’s strongest enforcement action against a technology empire that has come to embody China’s striking rise—and its founder Mr. Ma, a flamboyant celebrity businessman who has earned comparisons to Amazon.com Inc.’s Jeff Bezos.

The effort underscores Beijing’s resolve to rein in technology giants seen to be growing too quickly and, critics say, using their influence in ways that are reckless and disruptive to society.

Government investigators arrived at Alibaba’s Hangzhou campus on Thursday morning, according to people familiar with the matter. Alibaba and SAMR didn’t respond to requests for comment on the investigators.

The country’s antimonopoly regulator said in its statement Thursday that it was acting on reports that Alibaba was pressuring merchants who sell goods on its platforms to commit to not selling on its competitors’ platforms.

The practice has long been a bone of contention in China’s online retail industry, where Alibaba’s e-commerce platforms, Taobao and Tmall, compete with JD.com Inc. and Pinduoduo Inc. Alibaba’s domestic rivals have criticized the Hangzhou-based company for the practice, which a former senior Alibaba executive called “standard market practice†in a social media post last year.

Alibaba and Ant confirmed in separate statements that they had received notifications of the regulatory actions, and vowed to cooperate. Alibaba said that its businesses are operating as usual, while Ant said it would “seriously study and strictly comply with all regulatory requirements.â€

Mr. Ma couldn’t be reached for comment. He hasn’t appeared publicly since he criticized financial regulators for stifling innovation in an Oct. 24 speech that infuriated leader Xi Jinping and other senior officials. Mr. Xi personally instructed regulators to investigate risks posed by Mr. Ma’s business and to shut down Ant’s planned initial public offering.

JD.com and Pinduoduo didn’t reply to requests for comment.

Alibaba shares closed 8.1% lower in Hong Kong, while JD.com declined 2.3%. Alibaba’s rival Tencent Holdings Ltd.—which some investors believe could also get drawn into a broader regulatory crackdown—retreated 2.6% amid a slight gain in the broader stock market.

Regulators are zeroing in on whether Alipay, Ant’s payments platform, or other corners of Mr. Ma’s business empire have crossed the line into monopolistic behavior, according to a Chinese official with knowledge of the probes.

Alipay, in particular, has caught regulators’ attention because it possesses a wealth of data on the spending habits of hundreds of millions of Chinese consumers and businesses. The payments platform, housed under Ant, processed more than 118 trillion yuan, equivalent to $18 trillion, worth of transactions in mainland China in the year ended June 30.

Regulators are also worried that Ant’s online-lending model—which makes unsecured credit available to consumers and small businesses online—could potentially trigger “systemic risks†for China’s financial system, the official said.

Last month, Beijing pulled the plug on Ant’s planned IPO in Hong Kong and Shanghai, which was set to raise $34 billion in the biggest stock-market debut in history. Authorities also released draft regulations that would force the company to cough up more of its own capital to support its lending operations, or scale them back.

Since then, senior Chinese leaders have spoken publicly about limiting the market power of Chinese firms. Authorities also introduced new draft antitrust laws to restrict internet companies’ data collection and use, and measures to protect consumers.

The actions taken Thursday show that Beijing’s campaign to tighten oversight of domestic technology companies is still gathering steam.

The Chinese Communist Party’s flagship newspaper, the People’s Daily, wrote in a commentary Thursday that the new actions didn’t mean the state had changed its views toward encouraging the development of the internet platforms. But the commentary said that the actions were made “precisely to better regulate and develop the platform economy and to guide and promote its healthy development.†It said: “Without rules, nothing can be done.â€

Chinese internet firms have traditionally been allowed unfettered growth at home, as Beijing sought to develop its own national technology champions. Founded in 1999, Alibaba is perhaps the most powerful conglomerate of all, with business lines spanning e-commerce sites, cloud-computing services, entertainment and logistics. Alibaba and Tencent have long traded places as Asia’s most valuable company by market capitalization.

The recent moves by Beijing to tighten the reins on Alibaba and its peers put it, in one sense, into closer alignment with global regulators. In the U.S., where Facebook Inc. and Google parent Alphabet Inc. are facing antitrust cases, Silicon Valley executives argue that breaking up its giants would leave it vulnerable to competition by China’s tech giants. The current wave of actions could narrow that gap.

“China wants to get out in front, rather than deal later, with more hardened consequences, as the U.S. is struggling to do,†said Peter Fuhrman, Shenzhen-based chief executive officer of China First Capital, an investment bank. “A concern would be that market power may potentially morph into political power.â€

At the same time, any new regulatory oversight of the tech giants will likely be seen as part of Mr. Xi’s attempt to assert even more political control over the economy. He has sought to bring to heel private entrepreneurs and has talked regularly of needs to bolster government-run companies in key sectors such as finance.

In many ways, Ant acts like a financial institution by facilitating loans between banks and users of its ubiquitous Alipay payments app—used by one billion people in China—but it isn’t regulated like one. Its business model is structured in such a way that has been able to lure borrowers away from traditional lenders, while leaving the banks with the credit risk.

A White House-approved plan to transform TikTok into a U.S.-based company would keep the operation of the viral short-video app, and likely the algorithm that has powered its rise, in Chinese hands. This structure improves the deal’s chances of finding favor in Beijing, which had threatened to veto a sale.

President Trump said Saturday he had given his blessing to a deal that would see TikTok partner with Oracle Corp.  and Walmart Inc. to form a new entity called TikTok Global that would provide services to TikTok’s current users in the U.S. and most of the world outside China.

Under the terms of the deal, TikTok’s parent, Beijing-based ByteDance Ltd., would retain roughly 80% ownership of the new company, with Oracle and Walmart holding the rest, people familiar with the situation told The Wall Street Journal earlier. Because ByteDance is roughly 40% owned by U.S. investors, the new company, with the Oracle and Walmart stakes, could be described as having majority American ownership, they said.

At the same time, ByteDance’s 80% stake in TikTok would allay fears in Beijing that the White House was forcing China to relinquish one of the world’s hottest technology properties—or face a ban in the critical U.S. market.

At least in the short term, people close to the company and market observers described the arrangement as a win for China and for ByteDance.

A joint statement on the deal released Saturday by Oracle and Walmart didn’t mention any transfer of TikTok’s core algorithms, the artificial intelligence-driven content-recommendation engine widely acknowledged to be vital to its success.

Last month, Beijing imposed restrictions on the export of artificial-intelligence technology, in a surprise move that threw a monkey wrench into ByteDance’s negotiations with a handful of U.S.-based suitors. A person familiar with the company said the technology and core algorithms would be retained by ByteDance.

Trump’s signoff on TikTok’s deal with Oracle is a sign that the hardest part of the ordeal is over, though the U.S. government still has to process the details of the agreement, Zhang Yansheng, an economics professor at Renmin University, said Sunday. Beijing’s main concerns are about the sale of TikTok’s algorithm and U.S. ownership of the app, both of which seem to be addressed in the deal, he said.

“China will care about whether or not this company is still Chinese,†Mr. Zhang said.

Hu Xijin, the editor in chief of the Global Times, a Communist Party-backed tabloid, said the deal was unfair, but less costly for ByteDance than a full shutdown or sale of TikTok’s U.S. operations.

“The plan shows that ByteDance’s moves to defend its legitimate rights have to some extent worked,†he wrote in a commentary published Sunday. He also credited the Chinese government’s imposition of the technology export restrictions late last month with having led to a better outcome for Beijing.

Since the new limits were announced, ByteDance has discussed the potential sale in talks with both China’s internet regulator and the Ministry of Commerce, according to people familiar with the talks.

Still, the forced sale of a piece of one of the world’s hottest internet properties angered many in China, including Fang Xingdong, a former internet entrepreneur and founder of Beijing-based think tank China Labs, who described it in an interview Sunday as “daylight robbery.â€

The Chinese government hasn’t commented on the latest iteration of the deal or Mr. Trump’s endorsement of it. China’s Ministry of Foreign Affairs and Ministry of Commerce didn’t immediately respond to requests for comment.

The TikTok saga has rattled China’s government and technology industry. The app’s addictive content proved to be the perfect distraction for millions of people forced to stay home because of the coronavirus pandemic, turning it into the world’s hottest new social media sensation this year.

Just as its popularity was peaking, it got drawn into geopolitical tensions between Washington and Beijing, with Mr. Trump threatening to block it in the U.S. on national security grounds—unless it was sold to American buyers.

When China imposed the technology export restrictions, some analysts wondered whether a deal could be made that would satisfy both Washington and Beijing, not to mention ByteDance and any prospective American partners.

At stake was an app that has averaged roughly 7.6 million installations each month in the U.S. this year on Apple Inc.’s App Store and Alphabet Inc.’s Google Play store, with the peak of the frenzy coming in March, around the time of the start of the Covid-19 pandemic, according to data from Sensor Tower, an analytics firm.

The fight over TikTok served as a symbolic boon to China’s tech industry in that it showed the country is capable of creating a global tech asset that became the envy of Silicon Valley, said Peter Fuhrman, the Shenzhen-based chairman and chief executive officer of China First Capital, an investment advisory firm.

“The bottom line of what this means for China tech is soft power. It’s inspiration and affirmation that Chinese tech companies can achieve such heights,†Mr. Fuhrman said.

Even so, analysts warned that the episode would likely encourage Chinese companies to direct their focus inward, rather than pursue global expansion, given the geopolitical headwinds—a shift in mind-set that could have long-term implications for the Communist Party’s goal of turning the country into a global internet power.

TikTok’s troubles are likely to reinforce a shift already under way in China to focus more heavily on developing the country’s domestic market, in part as a response to a more hostile political environment abroad.

“For Chinese firms to survive and expand, an important life skill they will need to know is how to deal with such robbery, which is essential to protect themselves,†said Mr. Fang, the former entrepreneur.

Even if Chinese firms are forced to curb their overseas ambitions, there is still ample scope for expansion within China, said a senior executive at a Chinese technology giant, who declined to be named because of the sensitivity of the matter. Consumer demand in China’s smaller cities is still strong and growing, the person said.

Some analysts were less sympathetic, describing the blowback against TikTok’s global conquest as a natural response to Beijing’s own actions to block Facebook Inc., Twitter Inc. and other U.S. technology firms.

By erecting a wall around its own internet and shutting out foreign companies through censorship and investment restrictions, said Hosuk Lee-Makiyama, director of the Brussels-based European Center for International Political Economy, Beijing opened its companies up to these geopolitical concerns.

“Mainland China is now finally realizing there is a cost to pay for the Balkanization it created,†Mr. Lee-Makiyama said.

ByteDance Ltd. is considering changing the corporate structure of its popular short-video app TikTok, as it comes under increasing scrutiny in its biggest markets over its Chinese ties.

Senior executives are discussing options such as creating a new management board for TikTok or establishing a headquarters for the app outside of China to distance the app’s operations from China, said a person familiar with the company’s thinking.

TikTok, which has shot to global fame over the last two years thanks to its catchy dancing and lip-syncing videos, is owned by Beijing-based ByteDance, one of the world’s most valuable technology startups. ByteDance, whose secondary shares have valued the firm at $150 billion in recent weeks, counts big-name U.S. investors such as Coatue Management and Sequoia Capital among its backers.

The app has seen a surge in downloads as the coronavirus kept millions of people locked up in their homes and eager for distractions. About 315 million users downloaded TikTok in the first quarter of the year, the most downloads ever for an app in a single quarter, according to research firm Sensor Tower, bringing its total to more than 2.2 billion world-wide.

But as TikTok grows in popularity—and an increasingly assertive Chinese government raises hackles in foreign capitals—regulatory pressure on the app is intensifying.

Officials in several countries have expressed concerns with the large volumes of user data TikTok collects, with some speculating that ByteDance could be compelled to share it with the Chinese government. TikTok has repeatedly denied receiving Chinese government requests for user data and said it wouldn’t respond if asked.

The U.S. State and Defense departments already prohibit employees from downloading TikTok on government devices. On Tuesday, Secretary of State Mike Pompeo hinted at a possible ban for TikTok and other Chinese apps during an interview with Fox News.

In Australia, the chair of a legislative committee looking into foreign interference through social media named TikTok among the platforms that might be called to appear.

“What’s needed is a really clear understanding from the platforms about their approach to privacy and their approach to content moderation. That’s one of the objectives of this inquiry,†Jenny McAllister, the chairwoman of the committee, told an Australian radio station on Monday.

The government in India, one of TikTok’s largest markets, banned the app over cybersecurity concerns following violent clashes along the two countries’ disputed border.

Most recently, TikTok surprised observers by reacting more strongly than Western tech companies to Beijing’s imposition of mainland-style internet controls in Hong Kong.

“ByteDance is the first of China’s tech giants to make it big outside China, but the company that is the envy of China’s tech world is finding that success has a higher price perhaps than failure,†said Peter Fuhrman, the chairman of investment advisory firm China First Capital.

ByteDance managed to outperform its more established Chinese peers such as Alibaba Group Holding and Tencent Holdings in their quests to go global despite spending less on investments, he added.

ByteDance’s discussions about changing how TikTok is run are still in their early stages, but setting up an independent TikTok management board would allow a degree of autonomy from the parent company, the person familiar with the firm’s thinking said. This person wasn’t aware of any discussions around a corporate spinoff.

TikTok had also been considering opening a new global headquarters as early as December, The Wall Street Journal reported at the time. Singapore, London and Dublin were considered as possible locations. Recent events accelerated such plans, the person said.

TikTok currently doesn’t have a global headquarters. Recently installed Chief Executive Officer Kevin Mayer is based in Los Angeles.

The hiring in May of Mr. Mayer, a longtime Walt Disney Co. executive, put an American face on the Chinese company, whose website lists offices in 11 cities world-wide—none of them in China. The company says it doesn’t allow Chinese moderators to handle TikTok content.

ByteDance nevertheless has a long way to go to convince its critics. Any change to the corporate structure has to be significant enough to separate TikTok from any entanglements with mainland China, and has to cut off mainland Chinese staff from accessing user data, said Fergus Ryan, an analyst at the Australian Strategic Policy Institute. TikTok’s privacy policy says that user data can be accessed by ByteDance and other affiliate companies.

“Will the new structure be designed so as to remove any leverage Beijing can have over it? I find that hard to imagine,†Mr. Ryan said.

Drones spray disinfectant over South Korea. Police wear thermal imaging goggles to detect fevers in China. And a chatbot fields coronavirus questions in Australia.

The tech industry has long touted how ubiquitous connectivity, flashy gadgets and big data can improve people’s lives. The novel coronavirus epidemic is putting that bold promise to the test.

Health officials across Asia-Pacific, home to the first waves of virus contagion, have sought to repurpose existing technology to combat the fast-spreading virus. They are using smartphone-location tracking to piece together movements of suspected cases, developing government-run apps to monitor individuals’ health and keeping an eye on people’s temperature in the street with thermal goggles.

These new responses supplement traditional tactics such as quarantining sick people and canceling mass public events. But the tech-savvy tactics have yet to demonstrate broadly whether they are more game-changer than gimmick. Still, countries elsewhere might look to these solutions as the epidemic spreads.

The global number of confirmed coronavirus cases rose above 110,000 on Monday, according to data compiled by Johns Hopkins University, with infections found in 108 countries and regions.

In South Korea, the country hit hardest by the virus after China and Italy, the government rolled out a “Self-Quarantine Safety Protection” tracking app to keep digital eyeballs on the roughly 30,000 people officials told to stay home for two weeks. If a person brings their phone out of the permitted area, a mobile alert gets beamed to the individual and their government case officer.

In Singapore, a Southeast Asian country hit in the early stages of the virus outbreak, health officials are asking citizens to monitor their own movements with the QR code, the black-and-white bar code used for mobile payments. A scan of these codes, found in taxis, office lobbies, tourist attractions and colleges, bring people to a webpage where they are asked to input their names, contact details and on occasion declare their health status. The voluntary scans allow authorities to reverse engineer a citizens’ whereabouts in case they fall ill or come into contact with a patient.

In Singapore’s Nanyang Technological University, where students, staff and visitors scan such bar codes to leave a digital trail of the locations they visit in the university, the data helped the university probe whether any of their 33,000 students had come into contact with a cleaning contractor who worked in the school after that person was diagnosed with Covid-19, said Tan Aik Na, a senior vice president at the university.

The system has limits. Claudia Thong, a 21-year-old Singapore university student, scans QR codes pasted on the front doors and interiors of classrooms each time she attends lessons. Some students, however, can’t be bothered to scan the codes, she said. Faculty and staff have been asked to remind their students and guests to perform the QR code check-in, the university said in a statement.

Australia’s health department directs worried citizens to a virtual assistant named “Sam.” But inquiries for “coronavirus” go unrecognized, with the site suggesting the correct spelling is the two-word, “corona virus.” A follow-up question about anxieties relating to “corona virus” produced suggestions that had nothing to do with the respiratory illness.

The chatbot will soon be updated to refer people to Covid-19 resources, an Australian health-department spokesman said.

In China, where the largest Covid-19 outbreak has occurred, cities have deployed a variety of eye-catching technologies to diagnose and contain illness. Through measures such as social distancing and isolation, China has managed to limit the outbreak mostly to Hubei province, where the infectious disease emerged and where the majority of cases have occurred.

Unmanned aerial vehicles, typically used to spot forest fires or for police surveillance, can now scan crowds in China and spot someone hundreds of feet away running a fever, said Kellen Tse, deputy general manager for Shenzhen Smart Drone UAV Co., a drone company working with two Chinese provinces. The drone, which uses thermal imaging, sends alerts about those unwell to on-the-ground officials.

“China is unlike other countries,’ Mr. Tse said. “We have a large population, that’s why we’ve turned to technology to be more efficient.”

In Shanghai, digital devices are attached to the doors of those sequestered, according to the city’s state-television channel. People are allowed to go out to empty their trash and pick up deliveries, but unauthorized door movements trigger an alarm to the neighborhood police station, a policewoman told the broadcaster in an interview.

Chinese technology firm Baidu Inc. said this month that it helped develop an algorithm for Beijing subway officials to single out commuters not wearing masks. The image-recognition algorithm, which Baidu developed and tested seven days after a request from the city’s metro administration, runs on the video feeds from subway cameras and flags individuals without a mask or who don’t wear one properly.

Shenzhen, China’s tech-manufacturing center, requests that drivers entering the city scan a QR code and leave their contact details and travel history. Police officers wear thermal helmets and goggles to identify pedestrians who may be unwell, the Shenzhen government said on social media.

But the new-age tactics have their limitations. Commercial drones can only fly for about 20 minutes before needing a lengthy recharge, and the tech-heavy defenses are expensive, said Peter Fuhrman, a Shenzhen resident and chairman of China First Capital, a boutique investment bank. He credits the conventional response of the masses of volunteers and paid monitors deployed in Chinese neighborhoods with thwarting the virus.

“Fittingly, people, not machines, made all the difference here,” said Mr. Fuhrman, who has stayed in Shenzhen since the country’s outbreak began in January.

In South Korea’s hard-hit city of Daegu, private drone companies have been deployed to help disinfect public places at the local government’s request. A single drone can load around 2.5 gallons of disinfectant and spray an area of up to 105,000 square feet—or about the size of a typical Walmart store.

“It takes about 10 to 12 minutes to use it all up,” a Daegu city official said.

I’ve been here in Shenzhen, my adopted hometown, continuously from the start of the Coronavirus epidemic. While this city and the country are still confronting a monumental crisis and short-term economic uncertainty, the worst seems to be behind us. I want to say how grateful and inspired I am by the bravery, collective will and purpose, endurance and resolve of the Chinese people and its government. We fight and we prevail together

When John Zhao sealed the £900m takeover of the UK’s PizzaExpress in 2014 he burnished his reputation as a pioneer in China’s private equity industry. Two years later Hony Capital, his buyout firm, ploughed money into WeWork as the New York shared-office provider set its sights on an aggressive expansion in China.

Both deals shared a simple premise: take well-known western brands to China and they will flourish. “We have capital; we have a huge market to give access to,” Mr Zhao said shortly after the capture of PizzaExpress, which set a record for a Chinese buyout deal in the UK.

The acquisition was one of a wave of Chinese private equity investments over the past decade but few firms were as ambitious as Hony in their targets. Spun out of state-backed Legend Holdings in 2003, Hony shot to prominence through a series of restructurings of other state-owned groups. As it grew, so did its appetite for higher-profile, cross-border investments.

However, almost two decades on, Hony’s breezy confidence that China’s increasingly wealthy middle class would be ready-made consumers of all western brands has proved misplaced.

PizzaExpress restaurant openings in China have lagged behind an ambitious goal while local, lowercost competitors have lured customers away. Confidence that middle class would eat up imported names such as PizzaExpress prove misplaced.

This lacklustre start in China, combined with rising costs and a slowing casual dining market in the UK, left PizzaExpress with a £1.1bn debt pile that has set the scene for a restructuring battle between Hony and other bondholders.

After a calamitous 2019 in which WeWork was rescued by Japan’s SoftBank, its biggest backer, the New York-based company has ditched its leasing model in many cities, laid off thousands of staff and struggled with a particularly poor performance in China.

“The ‘can’t-miss’ strategy continues to do just that,” said Peter Fuhrman, chairman and chief executive at Shenzhen-based investment bank China First Capital. “Chinese investors and corporates have mainly fizzled when buying and localising western consumer brands.”

Other Hony investments — including the Beijing-based bike-sharing business Ofo, which collapsed in late 2018 — have soured, causing competitors to rethink importing western brands to China.

Chinese business history is littered with cases of western multinationals making the opposite mistake. UK retailer Marks and Spencer closed its Shanghai stores in 2017 after its combination of clothing and imported food confused local shoppers. US electronics retailer Best Buy retreated from China in 2014 after struggling to compete with cheaper domestic competitors.

But Chinese private equity groups appeared undeterred. They raised $230bn of capital between 2009 and 2014, according to investment bank DC Advisory.

Nanjing-based Sanpower largely flopped with its buyout of high-end retailer House of Fraser in 2014 and its failed attempt to expand the UK retailer across China. Bright Food, the state-owned Chinese group that bought a 60 per cent stake in Weetabix in 2012, failed to make the UK breakfast dish popular in China and eventually had to sell the brand in 2017.

“Four years ago everyone thought [buying foreign brands and bringing them to China] was the best thesis — but a lot of people got burnt,” said Kiki Yang, the partner leading Bain & Co’s Greater China private equity practice. “It’s not easy to bring something with no brand awareness to China. In reality, the success rate is very low.”

People who know Mr Zhao have said he was one of the first serious Chinese investors to have a solid grounding in the way deals were done in the US while also enjoying deep ties to state-owned groups, putting him in an enviable position at the advent of the Chinese private equity industry.

In its early days, that helped Hony become a rare channel connecting investors such as Goldman Sachs and Singapore’s Temasek with lucrative state deals that were otherwise inaccessible to foreign capital.

The PizzaExpress deal was a turning point for Hony and

other investors in the sector.

By 2014, the group had completed several successful cross-border deals, including an investment in Italian concrete producer Cifa. But the takeover of a popular British restaurant chain won instant global attention for Hony and Mr Zhao, who had spent most of the 1990s working at Silicon Valley technology companies such as Vadem and Infolio.

Hony’s investment in PizzaExpress came just as the UK’s casual dining market began to suffer from oversupply. It was also beginning to face stronger competition from local restaurants in China, a sign the UK brand name meant little to many Chinese diners.

PizzaExpress originally intended to open 200 outlets over a five-year period. So far it has launched about a dozen restaurants in the mainland, giving it a total of about 38, according to its website. In its annual results in April, the chain admitted it had “experienced challenges in China as we face intensifying competition from local brands”.

Without the promised growth in China to cushion the decline in the UK market, PizzaExpress has been pushed towards a debt restructuring process, cementing the deal’s position as an emblem of troubled Chinese investments overseas.

“Every time you say ‘China cross-border’, people think of PizzaExpress,” said one senior Chinese private equity executive. “It’s become a laughing stock — and bad for the reputation of China PE.”

PizzaExpress, Mr Zhao and Hony declined to comment.

As it seeks to resolve PizzaExpress’s problems, WeWork’s near collapse has inflicted further damage on Hony’s reputation. Hony and Legend Holdings led a $430m investment round in WeWork in 2016, and Mr Zhao became a member of WeWork’s board and later a consultant to its China business. SoftBank and Hony led a $500m investment round a year later.

With Mr Zhao acting as a consultant, WeWork expanded aggressively across the country, buying Chinese rival Naked Hub for $480m in cash and stock in 2018. Yet demand for office space fell in 2019, leaving some of its new areas of business virtually empty.

For example, in the western Chinese city of Xi’an, nearly 80 per cent of its desks were vacant, the FT reported in October. In the bustling start-up hub of Shenzhen in southern China, 65 per cent of its 8,000 desks were vacant.

WeWork declined to comment.

The poor performance of the business in China has left investors questioning how one of China’s private equity superstars could lead the group so far off course, according to people familiar with the matter.

“My impression is that Hony is not doing well these days,” said Liu Jing, a professor of accounting and finance at Cheung Kong Graduate School of Business in Beijing. “The economy has shifted to technology and they have lost their edge.”

Bytedance Inc. is considering setting up a global headquarters for its hit video-sharing app TikTok outside of China, part of continuing efforts to shake off its Chinese image, people familiar with the company said.

Singapore is one city being considered, the people said. Other possible locations include London and Dublin, with no American cities on the shortlist, one person said. TikTok currently doesn’t have a headquarters, although its most-senior executive is based in Shanghai and its main office, which runs U.S. operations, is in Los Angeles.

Senior executives at Beijing-based Bytedance—a startup valued at $75 billion, which owns numerous apps including TikTok—have been brainstorming ideas to rebrand TikTok as it comes under mounting scrutiny from U.S. lawmakers over national-security concerns. A headquarters outside of China would also bring TikTok closer to growing markets either in Southeast Asia or Europe and the U.S.

Known for its viral short videos of lip-syncing teenagers and funny pet antics, TikTok rose from obscurity to the top of U.S. app-store download charts in early 2019, and has also caught fire elsewhere including India and Japan. Global downloads for TikTok outstripped Facebook Inc. ’s Instagram and Snap Inc. ’s Snapchat in 2019, according to mobile-data aggregator App Annie. It had 665 million smartphone monthly active users world-wide in October, up 80% from a year earlier, App Annie said, with about 20 million of those users in the U.S.

The app’s spectacular rise has attracted attention from American senators, concerned that its Chinese roots could lead to it censoring content to appease Beijing. Bytedance’s 2017 acquisition of the startup Musical.ly, a move key to TikTok’s rapid success because of Musical.ly’s popularity in the U.S., is under review by the Committee on Foreign Investment in the United States for potential national-security risks.

The move to establish a global headquarters outside China has been discussed internally for months, one person said. However, the effort is “only accelerating because of the things happening in the U.S.,” the person added, referring to the recent scrutiny of TikTok there.

In response to questions, a TikTok spokeswoman didn’t directly address the search for a global headquarters, but said its teams around the world have increasingly been given more control over local operations.

“We have been very clear that the best way to compete in markets around the globe is to empower local teams,” she said. “TikTok has steadily built out its management in the countries where it operates.”

Locating TikTok’s headquarters outside China is unlikely to relieve pressures on Bytedance in the short term, said Peter Fuhrman, the Shenzhen-based chairman and founder of investment advisory firm China First Capital.

“That’s like dressing a panda in a business suit. It’s unlikely to fool anyone,” said Mr. Fuhrman, who described the firm as a victim of increased U.S.-China political tensions. “They’ll still be in congressional crosshairs and still subject to the same stringent content rules within China itself.” Bytedance has also faced pressures inside China from authorities seeking to restrict content deemed objectionable to the government.

In Singapore, the company has taken up two floors of prime office space in the city state’s central business district, according to real estate consultancy Savills Singapore. The 64,000-square foot space is in the same development housing investment advisory firm Rothschild & Co., and global banks such as UBS and Deutsche Bank. It first started operations in a WeWork office in downtown Singapore in December 2018.

Singapore is popular among foreign technology companies seeking a base in the region, with its large multilingual tech workforce and strong government support. It is the Asia-Pacific home to Alphabet Inc. ’s Google and Facebook, and Chinese technology giant Alibaba Group Holding Ltd. has a large presence there.

Southeast Asia is a top choice for Chinese companies looking to expand globally because of its cultural similarities, said Patrick Cheung, a founding partner at ZWC Partners and investor in Chinese tech startups.

A search on Bytedance’s hiring website on Dec. 23 showed 68 jobs posted for both Bytedance and TikTok in Singapore, the largest number of open positions for any city outside China. A fifth of those roles involved artificial-intelligence research as TikTok seeks to hire scientists in big data and natural-language processing. Bytedance uses AI to power some of TikTok’s recommendation algorithms. Other positions revolve around hiring staff to set content-moderation rules.

The global headquarters for another Bytedance product, a Slack-like corporate messenger app called Lark, is also in Singapore.

In London, where Bytedance was hiring for 38 positions including investment professionals and business-development staff, the company has made moves to poach talent. In October, TikTok hired Ole Obermann, a music industry veteran and former executive vice president at Warner Music Group, to head up its global music division.

Dublin stands out for pairing a favorable tax environment with a deep talent pool. Ireland’s capital is already the site of Facebook’s largest office outside of Menlo Park, and the European base for companies including Google and Twitter.

Bytedance acquired London-based AI music-composition startup Jukedeck this year. The startup’s founder and chief executive, Ed Newton-Rex, currently heads Bytedance’s new AI lab in Europe and wrote on LinkedIn last week that the team is hiring.

Bytedance launched TikTok in international markets in August 2017, modeling the service after its hit Chinese short-video app Douyin. Three months later, the company purchased Musical.ly, which started in China but grew popular in the U.S. It later merged the two apps.

—Yoko Kubota and Georgia Wells contributed to this article.

The inability of Chinese financial regulation to contain financial excesses has put off many foreign investors who would otherwise want to put their money into the country, analysts said.

The key problem is that Beijing has not yet found a way to meet the large demand by small private sector businesses, investors and entrepreneurs for credit through legal and regulatory compatible financing channels, analysts say. Until it does, it will continue to contend with a series of quasi-legal and highly speculative financing channels to meet that funding demand that will pose additional risks to the nation’s financial system.As the examples of the rise and fall of the shadow banking systems and peer-to-peer (P2P) lending platforms show, creative Chinese financiers will continue to push against – and, if needed, circumvent – the bounds of law and regulation to create highly lucrative ways to meet the capital demands of small businesses and investors.

Foreign investors also want to take advantage of the strong need for credit in China, but uncertainty over the regulatory environment has put many of them off.

“There is huge demand and private equity funds in the West are beginning to lend. However, they are demanding sky-high rates due to the huge risk of lending to private corporates in China that often have unstable funding and during a time of slowdown in China. For these reasons, only the larger funds with good research teams will jump in with any strength,†said Andrew Collier, managing director at Orient Capital Research.

Oaktree Capital Group, one of the world’s largest alternative investment firms, told the South China Morning Post last year it would continue to invest in distressed debt and equities in China despite the growth of sour loans.China’s latest efforts to overhaul its deeply troubled billion dollar P2P lending industry are unlikely to dampen the appetite for credit or tackle broader issues of debt and financial risk in the world’s second largest economy, analysts said.

“China’s private sector is as capital starved today as it has been perhaps for 20 years or more,†said Peter Fuhrman, chairman and chief executive of China First Capital, an investment bank based in Shenzhen. “So there are creditworthy Chinese borrowers habituated to paying what by international standards quite high interest [rates]. The challenges remain not inconsiderable. At the top of the list is tougher government regulation on nonbank lending.â€

Investors in Chinese online peer-to-peer lender Ezubao chanting slogans during a protest in Beijing after the platform turned out to be a giant Ponzi scheme. Photo: AFP

Beijing has taken steps to tighten regulation of P2P platforms since 2015 amid a spate of high-profile company collapses and scandals that have rocked the industry and trapped the savings of millions of people.

The internet-based lending platforms match private investors with individuals and small companies that want to borrow, providing a lifeline for entities that have trouble accessing the traditional banking system.

The number of mainland P2P lenders has shrunk significantly over the past four years, from some 6,000 platforms operating in 2015 to just 572 in October this year, according to P2P tracking portal Waidaizhijia. But although the industry’s reputation for risky lending has attracted greater regulatory oversight, P2P lending continues to play an important role in China’s economy.

“P2P has looked like an attractive way to get capital to smaller firms and to regions of the country that have low access to bank lending,†said Collier.

“However, most of the money is going into speculative investments in property, along with established securities such as the better grade corporate bonds. The regulators go back and forth on how much freedom they want to give to this sector.â€

To tackle financial risks in the banking system, China has already taken a hard stance against shadow banking, which often involves many forms of off-balance-sheet lending from banks and nonbank financial firms, by rolling out new regulations to focus on supervising asset management businesses and products of commercial banks.

So far China’s effort seems to have made a significant difference to slowing the growth of the shadow banking industry. Rating agency Moody’s estimated that broad shadow banking assets shrank by nearly 1.7 trillion yuan (US$242 billion) in the first half of 2019 to 59.6 trillion yuan (US$8.4 trillion), the lowest level since the end of 2016.

Broad shadow banking assets declined only slightly to 64 per cent of nominal gross domestic production (GDP) at the end of June 2019 from 68 per cent at the end of 2018. But they were down 23 percentage points compared to the peak of 87 per cent of GDP at the end of 2016, Moody’s said.

Despite the crackdown by authorities, P2P lenders are likely to continue filling an important gap in the Chinese economy, according to analysts, although growth would be slower than during 2014 to 2018. Consultants Frost & Sullivan forecast P2P lending to grow in value to 2.17 trillion yuan (US$309.4 billion) by 2023, compared to 789 billion yuan (US$112 billion) in 2018.

“The explosive growth of the P2P industry since 2010 confirms there is huge and unmet demand for capital,†said Fuhrman. “Especially among smaller Chinese private sector companies.â€

People protest over losses incurred in peer-to-peer investment schemes in front of the public security ministry of Dongcheng district in Beijing. Photo: Reuters

Part of the problem is that China’s banking system has not evolved to meet the demands of the private sector, which has been the engine of the country’s economic growth. Commercial banks prefer to lend to state-owned enterprises, which have implicit government backing, and are reluctant to lend to private companies because they are seen as being less creditworthy.

“In the past, non-performing [loans] were very high, so lending to small firms was discouraged,†Tian Guoli, the chairman of China Construction Bank, the country’s second biggest lender, said last year.

Squeezed between interest rates at P2P platforms that can be up to four times that charged by Chinese banks, and weak prospects of borrowing from large lenders, many small private companies have struggled to stay on top of debt.

The problem has been particularly acute through formal lending mechanisms such as the bond market. Between January and October this year, 93 private firms have defaulted on 278.7 billion yuan (US$39.6 billion) worth of Chinese bonds.

The overall default rate has now hit 1.51 per cent, a record high for the Chinese bond market since 2014, according to a report published by investment bank China International Capital Corporation last Friday. The default rate of a bond issued by a Chinese private company hit 11.82 per cent this year, nearly doubling from 6.18 per cent in 2018 and more than six times the rate of 1.89 per cent in 2017.

“While the overall liquidity in onshore bond market has improved, weak issuers will continue to face refinancing pressure over the next 12 months, because investors will remain risk averse towards them,†said Ivan Chung, an associate managing director at rating agency Moody’s.

The People’s Bank of China has called for risks associated with the P2P industry to be resolved by the first half of 2020, while some provinces like Hunan in central China have moved to ban the platforms altogether.

However, analysts said that given that much of China’s private sector is in need of cash to repay debt, the industry was unlikely to disappear, even amid growing regulatory scrutiny.

“It’s better to have greater transparency and regulatory oversight,†said Fuhrman. “The lending doesn’t stop, but the money becomes more expensive and risky for borrowers. This has a deadweight cost to the Chinese economy. The sooner the legitimate nonbank lending sector gets cleaned up and back in business the better it will be for China as a whole.â€

Enterprise Ireland, the Irish government export development agency, held a conference in Dublin earlier this month to promote more intensive collaboration between businesses in Ireland and China, particularly in high-technology. I was invited to give a keynote speech, titled “China and Ireland: Building a Powerful High-Tech Partnership”. You can watch the first six minutes by clicking here.

Many thanks to my friend and amateur cinematographer Elaine Coughlan, an Enterprise Ireland board member as well as managing partner at Altantic Bridge Capital. Elaine has an outstanding track record as a tech entrepreneur and investor, in Silicon Valley, Ireland and China. I was also honored to be on a panel Elaine moderated.

Ireland is the only country in the European Union that has a trade surplus with China. The country stands to benefit greatly from Brexit, as international tech companies move European operations out of the UK and to the only EU Eurozone country with English as its native language. Two other big plusses: Ireland is a business-friendly place with about the lowest corporate taxation rates around.

Enterprise Ireland has a great team in China, led by Mary Kinnane, Tom Cusack and Patrick Yau. I met executives from two of Ireland’s success stories in China, Decawave and Taoglas.

Investment banks bringing companies to list on China’s new board for technology startups are facing an unusual requirement: they will have to keep some of the shares for themselves.

The Shanghai Science and Technology Innovation Board marks a major experiment in the reform of China’s capital markets.

Chinese President Xi Jinping announced plans in November for a Nasdaq-style board for young tech startups, and it is expected to be operational later this year. It aims to attract young companies with fewer regulations and reporting requirements and, unlike China’s main markets, there are to be no limits on pricing and first-day trading movements.

Also unlike the country’s existing boards in Shanghai and Shenzhen, companies that list do not have to be profitable. In some cases, the tech board will not even require companies to have generated revenue.

The board signifies the realization of long-discussed plans to move from a system where Chinese regulators carefully review every applicant and maintain tight control over the flow of listings — leading to a backlog of hundreds of companies waiting years for an official nod — to a more market-driven system like that of major foreign exchanges.

The requirement that underwriters take a stake in initial public offerings, first flagged by officials last month, is an indicator of the authorities’ caution; members of the Chinese financial community say the stakeholding requirement is intended to insure underwriters bring only the companies in which they have confidence to market.

“Having lowered profitability requirements, it further makes sense to have sponsors with skin in the game,” said Brock Silvers, managing director of investment company Kaiyuan Capital in Shanghai.

Executives with two Chinese financial companies said the minimum stake will be “a low single-digit” percentage of the IPO. A lock up rule will block the underwriters from selling their shares within two years of the IPO. The rules have yet to be formally issued.

Victor Wang, executive director of financial sector research at China International Capital Corp., the country’s largest investment bank, said it is still unclear how the stakeholding requirement will be shared among different investment banks involved in an IPO. But the logic is, “if you don’t focus on quality and recommend some low-quality companies, you own money will be lost,” he said.

China Merchants Securities, which is sponsoring two companies preparing to list on the new board, declined to comment about the new rule. However, a local broker, who had not heard of it before, said he was not surprised at the requirement.

“China’s financial legal framework is not flawless and officials at the China Securities Regulatory Commission cannot completely trust sponsors’ due diligence work,” he said. “After all, there have been IPO frauds before. It is no surprise if regulators want some level of assurance by having brokers to share risks.”

Some market observers are wary of the consequences, however.

“The intention is a good one but once again investors are not being forced to make their own decisions and analysis,” said Fraser Howie, a veteran broker and co-author of three books on Chinese financial markets. “By forcing the (investment bank) to come in on every deal, it effectively tells investors, ‘Don’t worry. You don’t need to think for yourselves’.”

Howie also sees the rule as problematic for the banks. “The investment bank’s job is to bring a company fairly to market,” he said. “I think this (rule) conflicts with this. To me, they are creating a needless conflict of interest and additional risk for the bank.”

The burden of the requirement will favor larger investment banks, in the view of Yang Yingfei, a partner handling IPOs at Baker McKenzie FenXun Joint Operation Office in Beijing.

“Sponsors that are relatively stronger overall will become more competitive, whereas small and medium-sized securities firms may gradually lose the ability to sponsor tech board enterprises,” she said. “The effect of concentration in the sector will become conspicuous.”

Though the Innovation Board’s approach is unusual, other market regulators have also been wrestling with the question of how to ensure that underwriters take responsibility for companies they bring to market.

Last month, the Securities and Futures Commission of Hong Kong reprimanded and fined UBS, Merrill Lynch, Morgan Stanley and the securities arm of Standard Chartered Bank over their handling of IPOs.

UBS received the heaviest penalty, a fine of 375 million Hong Kong dollars ($47.78 million) and a one-year suspension from sponsoring listings on the Hong Kong market. The SFC said the bank had failed to confirm the existence of key claimed assets and customers of China Forestry Holdings before bringing it to market in 2009 and found problems with its work on two other IPOs.

China Forestry raised $216 million in its IPO but its shares stopped trading in 2011 after its auditor reported the discovery of accounting irregularities.

Preparations for the Shanghai Innovation Board have moved unusually quickly since it was first mooted in November. The authorities are keen to have “unicorns” — unlisted startups valued at $1 billion or more — list on domestic markets rather than offshore. After several abortive efforts, they are hoping they have created an attractive alternative at last.

As of yet, the country’s most valuable companies, online services companies Alibaba Group Holding and Tencent Holdings, are listed in New York and Hong Kong, respectively.

“There are certainly signals that the tech board’s IPO procedures will be more market-driven, with a less onerous process of CSRC approval and monitoring,” said Peter Fuhrman, chairman of investment bank China First Capital in Shenzhen. “That should be a positive development.”

Nine companies are set to launch on the new board as soon as June, but none are unicorns; combined, they are expected to raise only about $1.6 billion. Financiers say bigger startups are waiting for the board to work through its initial launch pains before moving forward themselves.

One Hong Kong-based banker who works with mainland Chinese companies said “a lot” of his clients were waiting in the wings.

A Chinese education company backed by U.S. investors including Kobe Bryant is cracking down on how its Western teachers cover politically fraught topics.

VIPKid, one of China’s most valuable online education startups, has put hundreds of its mostly American teachers on notice for using certain maps in their classes with Chinese students, and has severed two teachers’ contracts for discussing Taiwan and Tiananmen Square in ways at odds with Chinese government preferences,people familiar with the company say. Since last fall, teachers’ contracts state that discussing “politically contentious” topics could be cause for dismissal, according to one reviewed by The Wall Street Journal.

The moves highlight the balance a Chinese company must strike in fulfilling global aspirations while toeing Beijing’s line. Five-year-old VIPKid is currently in talks to raise as much as $500 million in new funding from U.S. and other investors that could value the company at roughly $6 billion, people familiar with the fundraising said.

“A company must keep good relations with the government and ideology,” said Peter Fuhrman, chief executive of investment firm China First Capital . “But that can cause friction when you’re also courting foreign investors, expanding business overseas and employing a large American workforce.”

Beijing-based VIPKid says it has more than 60,000 teachers in the U.S. and Canada who teach English to more than 500,000 children ages 4 through 15, who live mostly in China. Teachers work as independent contractors and can earn between $14 and $22 an hour. They must have a bachelor’s degree, at least one year of teaching experience and eligibility to work in the U.S. or Canada.

Curricula are provided, and teachers give English-language instruction, sometimes using geography or historical figures. VIPKid’s approach is consistent with maps and materials in the Chinese education curriculum, which calls Taiwan a part of China. Textbooks don’t mention the military’s suppression of the Tiananmen Square pro-democracy demonstrators in 1989, and discussion of it is forbidden.

A spokesman said VIPKid has “an elevated level of responsibility to protect the safety and emotional development of the young children on our platform.” The company expects teachers to understand cultural expectations, he said, adding it had to “make a difficult decision” to terminate the contracts of “an exceptionally small number of teachers” who “decided to ignore the needs of their students” and “the preference of their parents.”

Chinese education technology attracted $5.3 billion in investment last year, double the amount a year earlier, according to Dow Jones VentureSource data. VIPKid’s investors include U.S. hedge-fund firm Coatue Management LLC, venture-capital firm Sequoia Capital, Chinese social giant Tencent Holdings Ltd. and a venture fund co-launched by retired NBA star Kobe Bryant.

The company’s actions have rankled some teachers. Typically, these instructors have displayed maps of the world, including China, that they found on their own. Starting last fall, hundreds began receiving emails or calls from VIPKid stating their maps weren’t aligned with Chinese education standards, people familiar with the matter said. Teachers who refuse to adhere to the map standards could have their contracts terminated, after conversations with VIPKid. Map-related dismissals haven’t happened, said a person familiar with the company.

Will Rodgers, a 26-year-old American teacher based in Thailand, said he discussed Tiananmen Square twice during VIPKid lessons about famous Chinese landmarks. First, he told a 12-year-old student “the Chinese government jailed and killed many people just for protesting.” He then showed a 15-year-old student photos and video footage of the protest, and his contract was terminated. Mr. Rodgers said he doesn’t agree with VIPKid’s stance, but doesn’t blame the company for ending his contract.

Another American teacher’s contract was terminated earlier this year after he told students that Taiwan was a separate country, according to people familiar with his case. A third teacher received a call from VIPKid after telling a student that Tibet, an autonomous region in China with a history of separatist activity, is a country, during a lesson on China’s neighbors, according to a person familiar with the matter. He was told on the call he should refer to Tibet as part of China.

People familiar with VIPKid say it monitors classes for missteps over political content. Another person familiar with the matter said the company uses artificial intelligence to determine material students find engaging and to protect them from inappropriate behavior.

Some teachers and VIPKid investors say that education from foreign teachers, even if it is screened, can benefit students because they get exposed to other cultures. Rob Hutter, a founder and managing partner of Learn Capital, an early investor in VIPKid, said the company is trying to take a common-sense approach by teaching uncontroversial content.

“No matter what nation you’re teaching in, there are going to be things that we need to be thoughtful about,” he said. “Even in American classrooms, there are things you cannot discuss.”

“No matter what nation you’re teaching in, there are going to be things that we need to be thoughtful about,” he said. “Even in American classrooms, there are things you cannot discuss.”

Fundraising by renminbi-denominated private equity groups in China plummeted 86 per cent last year, squeezed by a tighter availability of credit and a slower initial public offering market.

The fall — revealed in a new report published on Friday — underlines how the Chinese private equity market has gone into reverse from the boom times of a few of years ago, when scores of new funds were launched and the country’s technology companies attracted sky-high valuations.

Hundreds of small, inexperienced Chinese private equity funds that rushed into investments in technology and new economy companies have begun to suffer from a sharp contraction in fundraising and tougher environment for exiting investments.

Private equity houses raised about $13bn in renminbi-denominated funds in 2018, down about 86 per cent from the $93bn raised the year before, according to data compiled by the consultants Bain & Co.

At the same time, small Chinese private equity groups struggled to cash in on their investments in 2018. Sales and initial public offerings worth less than $100m fell by about 64 per cent last year compared to a five-year average.

“The level of optimism and fervour for investing in the tech sector foreshadowed what we are seeing now,” said Usman Akhtar, a partner at Bain & Co, referring to how many small private equity houses are struggling to exit from investments at expected prices. “It’s the start of this and it may take a few years to pan out.”

The tightening of credit in China is a broad trend with an impact far beyond private equity. Banks, trusts and other sources of capital have been squeezed during China’s attempt to slow the growth of debt.

So-called shadow banking has been an important source of funds for small private equity groups. Without these channels to fresh cash, many of the imperilled funds are simply shutting down, raising doubts over whether investors will be paid.

China’s woes are mirrored across Asia where large private equity is sucking up most of the available capital while also finding means to exit their investments, Mr Akhtar said. Hong Kong-based PAG, which is run by former TPG and JPMorgan executive Shan Weijian, raised a $6bn fund in November, following a more than $9bn fund raised by Hillhouse, the Beijing and Hong Kong-based group.

Large exits of more than $500m clearly diverged from smaller deals in 2018 by rising just over a quarter on the year before.

Global demand for Chinese technology IPOs started 2018 with a bang but quickly showed signs of fizzling out, leading to a bottleneck of private equity seeking to exit their investments.

Over the past year several large, private equity-backed groups have been forced to scale back their IPOs or delay them indefinitely.

Tencent Music, which is partly owned by private equity, was last year targeting a $4bn float but ended up raising only $1.1bn after several delays.

“The reality is that all PE and VC investing in China has been an unhedged bet that the IPO process in China would liberalise and institutional investors in US and Hong Kong would show consistent, strong interest in Chinese IPOs. Neither is true,” said Peter Fuhrman, chairman of China First Capital, a Shenzhen-based investment bank.

In splendid Dubai to attend the Global Investment in Aviation Summit and share data and outlook for China’s fast-growing and even faster-evolving aviation sector.

My thanks to the kind invitation from the United Arab Emirates General Civil Aviation Authority. Anyone flying in and out of the Emirates will know that it is a benchmark for worldwide best practices in aviation and airport management.

Someday, I’d like to see the UAE’s second largest export to China, after petroleum products, will be aviation services, consulting, management.